Clear Maximizing Value Finances

Insurance Explained: How to Safeguard Your Wealth and Tomorrow

Understanding insurance is crucial for all people who wants to secure their financial stability. Insurance offers a safeguard against unexpected events that could lead to significant losses. A wide range of coverage options exists, tailored to meet specific requirements. Yet, numerous people find it difficult figuring out the necessary extent of coverage and navigating the specifics of their policy. The complexities of insurance can create uncertainty, prompting the need for a clearer understanding on how best to protect one's wealth. What factors should people weigh before making a decision?

Fundamental Insurance Concepts: Key Principles

Insurance functions as a monetary safeguard, protecting individuals and businesses against unexpected dangers. It is fundamentally a contract linking the customer and the company, where the insured pays a premium in exchange for financial coverage covering defined damages or setbacks. At its core, insurance is about handling risk, enabling people to shift the responsibility of possible monetary damage onto a provider.

Insurance policies outline the terms and conditions, explaining which events are included, what is excluded, and the procedures for filing claims. Resource pooling is fundamental to coverage; numerous people contribute to the scheme, making it possible to finance payouts to those who incur damages. Grasping the core concepts and language is crucial for choosing wisely. Ultimately, insurance intends to give reassurance, ensuring that, in times of crisis, people and companies are able to bounce back and maintain their prosperity.

Different Forms of Coverage: A Detailed Summary

Many different kinds of insurance exist to address the wide-ranging necessities of individuals and businesses. Key examples are medical insurance, designed to handle doctor bills; motor insurance, shielding against automobile harm; and homeowners insurance, safeguarding property against hazards like burning and robbery. Term insurance grants fiscal safety for dependents if the insured passes away, whereas income protection offers salary substitution if one becomes unable to work.

In the corporate sector, liability coverage guards from accusations of wrongdoing, and asset insurance secures physical holdings. Professional liability insurance, or simply errors and omissions insurance, protects professionals from claims resulting from errors in their work. Additionally, travel coverage insures against unanticipated situations while traveling. All insurance policies is crucial for risk management, ensuring individuals and businesses can mitigate potential financial losses and maintain stability in uncertain circumstances.

Determining What Insurance You Need: What Level of Protection is Sufficient?

Figuring out the right degree of necessary protection demands a thorough assessment of property value and possible dangers. People need to evaluate their financial situation and the property they want to safeguard to arrive at an adequate coverage amount. Sound risk evaluation methods are crucial for making sure that one is not insufficiently covered nor paying extra for needless protection.

Assessing the Worth of Assets

Evaluating asset value is a crucial stage in knowing the required level of protection for sound insurance safeguarding. This step entails establishing the price of private possessions, real estate, and investment portfolios. Those who own homes need to weigh factors such as today's market situation, reconstruction expenses, and depreciation when appraising their property. Also, people need to assess personal belongings, automobiles, and any liability risks linked to their possessions. Through creating a comprehensive list and appraisal, they are able to pinpoint possible holes in their protection. In addition, this assessment assists people tailor their insurance policies to suit unique requirements, ensuring adequate protection against unanticipated incidents. In the end, accurately evaluating asset value lays the foundation for smart coverage choices and financial security.

Risk Assessment Strategies

Gaining a comprehensive grasp of asset value naturally leads to the next phase: determining necessary insurance. Risk evaluation techniques entail recognizing future dangers and determining the appropriate level of coverage needed to lessen those hazards. The evaluation commences with a comprehensive list of possessions, including homes and land, cars, and personal belongings, alongside an analysis of potential liabilities. The individual must consider things such as location, daily habits, and industry-specific risks that could impact their insurance requirements. In addition, examining current policies and finding coverage deficiencies is essential. By measuring potential risks and matching them to asset worth, it is possible to make sound judgments about the required insurance type and quantity to secure their future reliably.

Grasping Policy Language: Core Principles Defined

Understanding policy terms is vital for traversing the complexities of insurance. Core ideas like coverage categories, insurance costs, deductibles, policy limits, and restrictions are important elements in determining the effectiveness of a policy. A clear grasp of these terms helps individuals make informed decisions when choosing coverage plans.

Types of Coverage Defined

Insurance policies come with a selection of different coverages, each designed to address specific risks and needs. Typical categories involve coverage for liability, which shields from legal action; property coverage, protecting physical possessions; and coverage for personal injury, which addresses injuries sustained by others on your property. Furthermore, comprehensive coverage gives defense against a broad spectrum of dangers, including theft and natural disasters. Specific insurance types, such as professional liability for businesses and health insurance for individuals, customize the coverage further. Grasping these categories assists clients in selecting appropriate protection based on their individual needs, ensuring adequate protection against potential financial losses. Each form of protection is essential in a comprehensive coverage plan, leading to financial security and peace of mind.

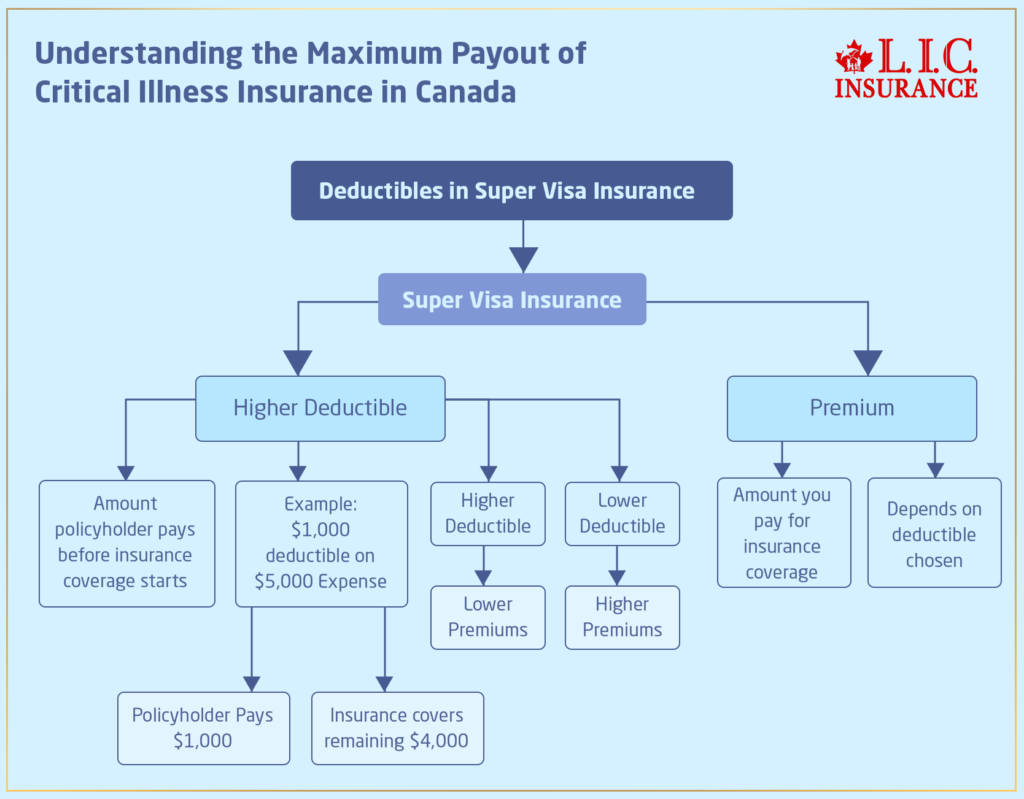

Premiums and Deductibles

Choosing the appropriate coverage categories is only part of the insurance equation; the financial components of premiums and deductibles heavily affect policy selection. Premiums are the expense associated with keeping an insurance policy, generally paid on an annual or monthly basis. A higher premium often correlates with more extensive coverage or reduced out-of-pocket costs. Conversely, deductibles are the sums the insured must cover personally before their insurance coverage kicks in. Choosing a higher deductible can lower premium costs, but it could result in more fiscal liability during claims. Grasping the relationship between these two factors is essential for individuals seeking to safeguard their possessions while managing their budgets effectively. Ultimately, the relationship of deductibles and premiums determines the overall value of an insurance policy.

Coverage Limits

What elements that can reduce the utility of an insurance policy? Exclusions and limitations within a policy outline the situations under which coverage is withheld. Standard exclusions include pre-existing conditions, war-related incidents, and certain types of natural disasters. Restrictions can also pertain to defined benefit levels, necessitating that policyholders grasp these restrictions thoroughly. These elements can considerably affect claims, as they determine what damages or losses will not be compensated. It is vital that policyholders examine their insurance contracts carefully to spot these limitations and exclusions, making sure they fully understand about the limits of their policy. A clear grasp of these terms is crucial for protecting one's wealth and future financial planning.

Filing a Claim: What to Expect When Filing

Making a claim can often be confusing, particularly for individuals new with the process. The initial step typically is to alert the insurance company of the incident. This can often be accomplished through a telephone call or online portal. Once the claim is reported, an adjuster may be designated to review the situation. This adjuster will examine the specifics, gather necessary documentation, and may even go to the incident site.

After the assessment, the insurer will decide on the legitimacy of the claim and the compensation due, based on the contract stipulations. Those filing should be prepared to offer supporting evidence, such as documentation or images, to facilitate this evaluation. Communication is essential throughout this process; you may have to contact with the insurer for updates. Ultimately, understanding the claims process allows policyholders to manage their rights and responsibilities, making sure they get the payment they deserve in a timely manner.

Tips for Choosing the Right Insurance Provider

How does one find the most suitable insurance provider for their needs? To begin, people must evaluate their particular needs, taking into account elements such as policy varieties and financial limitations. It is crucial to perform comprehensive research; internet testimonials, ratings, and client feedback can provide a view into customer satisfaction and the standard of service. In addition, obtaining quotes from multiple providers enables comparisons of premiums and policy details.

It is also advisable to evaluate the financial stability and credibility of potential insurers, as this can affect their capacity to pay claims. Talking with insurance professionals can help explain the policy's rules, ensuring transparency. Moreover, seeing if any price reductions apply or package deals can enhance the overall value. Lastly, getting suggestions from people you trust may lead to discovering dependable choices. By following these steps, consumers can select knowledgeably that are more info consistent with their insurance needs and financial goals.

Staying Informed: Ensuring Your Policy Stays Relevant

After selecting the right insurance provider, policyholders should be attentive about their coverage to make certain it addresses their changing requirements. Regularly reviewing policy details is essential, as major life events—such as getting married, buying a house, or career shifts—can change necessary policy levels. Individuals should schedule annual check-ins with their insurance agents to discuss potential adjustments based on these life events.

Furthermore, staying informed about industry trends and changes in insurance regulations can give helpful perspectives. This information might uncover new coverage options or discounts that could enhance their policies.

Keeping an eye on the market for better prices may also result in cheaper options without reducing coverage.

Commonly Asked Questions

In What Ways Do Insurance Costs Change With Age and Location?

Insurance premiums typically increase with age due to higher risk factors associated with senior policyholders. Additionally, geographic area influences costs, as urban areas often experience higher premiums due to more risk from crashes and stealing compared to non-urban locations.

Am I allowed to alter my current insurer before the policy expires?

Certainly, policyholders may alter their insurer during the policy term, but it is necessary to check the conditions of their current policy and guarantee they have new coverage in place to prevent periods without insurance or possible fines.

What occurs if I fail to make a insurance installment?

If an individual misses a scheduled installment, their insurance coverage may lapse, leading to potential loss of protection. The coverage might be reinstated, but could require back payments and may involve penalties or higher rates.

Do pre-existing medical issues qualify for coverage in health plans?

Pre-existing conditions may be covered in health plans, but the inclusion depends on the specific plan. Numerous providers enforce a waiting time or limitations, while others may provide immediate coverage, highlighting the need to check policy specifics carefully.

How Do Deductibles Affect My Insurance Costs?

The deductible influences coverage expenses by determining the amount a holder of the policy is required to spend before coverage kicks in. A larger deductible generally means reduced monthly payments, while lower deductibles lead to higher premiums and potentially less out-of-pocket expense.